Top Rated Course

Top Rated Course

We may not have the course you’re looking for. If you enquire or give us a call on 01344203999 and speak to our training experts, we may still be able to help with your training requirements.

Basel II vs. Basel III: Detailed Comparison

Eliza Taylor 21 February 2025Dive into the world of "Basel III Implementation" and gain a comprehensive understanding of Basel III, exploring its associated challenges and considerations. This informative blog takes you through the vital changes in banking regulations and the timeline for adoption. By the end, you'll have a solid grasp of Basel III's impact on the financial industry.

Training Outcomes Within Your Budget!

We ensure quality, budget-alignment, and timely delivery by our expert instructors.

In the realm of global financial regulation, the Basel framework has played a pivotal role in shaping the stability and resilience of the banking sector. Basel II and Basel III stand as two significant iterations of this framework, each evolving to address the lessons learned from financial crises and changing market dynamics. However, it is only natural to wonder the comparison between Basel II vs Basel III and why the framework needed to be updated and upgraded.

According to a report by The Financial Times, around 7.8 trillion GBP, more than a sixth of the global Gross Domestic Product (GDP) in 2008 was lost during the financial crisis. While Basel II was already in place at the time, it failed to stop a catastrophe of that magnitude. This blog undertakes an in-depth comparison of Basel II vs Basel III, delving into their key features, differences, and their collective impact on the global banking landscape.

Table of Contents

1) Understanding Basel II vs Basel III

2) Basel II vs Basel III: Key features

3) Differences between Basel II and Basel III

4) Impact on the banking landscape

5) Conclusion

Understanding Basel II vs Basel III

Before diving into the dichotomy between Basel II and Basel III let’s first understand the frameworks and the way they work.

Basel II: Building Risk Management

Introduced in 2004, Basel II represented a significant shift in banking regulations. It aimed to address the limitations of its predecessor, Basel I, by focusing on the sophistication of Risk Management within financial institutions. Basel II introduced the concept of Risk-weighted assets, acknowledging that not all assets carry the same level of risk.

This allowed banks to allocate capital more accurately based on the riskiness of their portfolios. The framework was segregated into three pillars: Minimum Capital Requirements, Supervisory Review, and Market Discipline. These pillars aimed to enhance Risk Management practices, regulatory oversight, and market transparency.

Basel III: Enhancing resilience

Post the 2008 financial crisis, Basel III framework was put forward as a response to the vulnerabilities exposed during the turmoil. Introduced gradually from 2010, Basel III went beyond Basel II's focus on Risk Management. It aimed to build resilience and stability in the banking sector. The framework introduced higher Minimum Capital Requirements and, Critically Capital Buffers. These buffers act as cushions during economic stress, making sure that banks have sufficient capital to absorb losses. Basel III also introduced Liquidity Standards like the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) to address Liquidity risks.

In essence, while Basel II refined Risk Management practices, Basel III goes further by enhancing the ability of banks to weather adverse scenarios. These two iterations of the Basel framework reflect the evolution of regulatory philosophy from purely Risk Management to a comprehensive approach that prioritises resilience and stability in the face of a rapidly changing financial landscape.

Basel II vs Basel III: Key features

After the 2008 financial meltdown, Basel II’s shortcomings gave rise to Basel III. Here, we’ll take a look at the key features that separate the two.

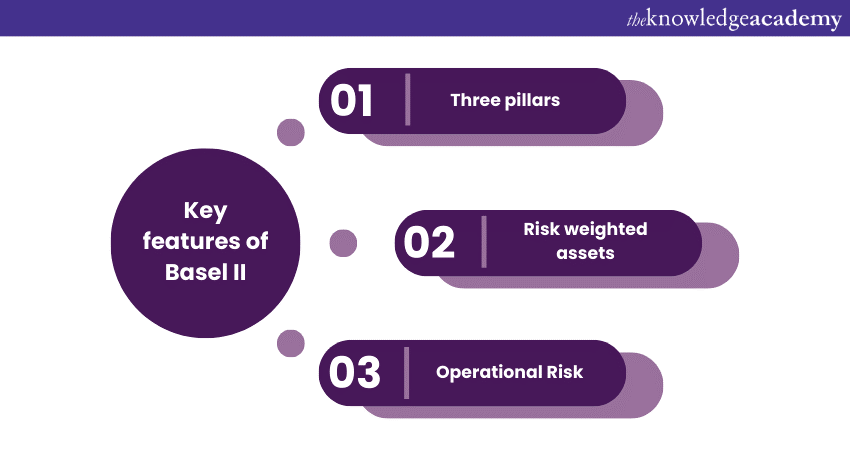

Key features of Basel II

a) Three pillars: Basel II was structured around three pillars: Minimum Capital Requirements, Supervisory Review, and Market Discipline. This framework aimed to enhance Risk Management, regulatory oversight, and transparency.

b) Risk weighted assets: Basel II introduced a more nuanced approach to capital requirements by assigning Risk Weights to different asset classes. Banks were required to hold capital proportional to the risk inherent in their portfolio.

c) Operational Risk: Basel II recognised Operational Risk as a distinct category and introduced methods for calculating Capital Requirements based on a bank's exposure to Operational Risks.

Key features of Basel III

a) Capital Buffers: Basel III emphasised Capital Buffers, including the Capital Conservation Buffer, the Countercyclical Capital Buffer, and the Systemically Important Banks (SIB) Buffer. These buffers bolster a bank's ability to withstand economic downturns.

b) Liquidity Standards: Basel III introduced Liquidity Standards like Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) to ensure banks maintain sufficient Liquidity to weather short-term and long-term stress.

c) Leverage Ratio: Basel III introduced a Leverage Ratio to prevent excessive borrowing and ensure banks maintain a reasonable balance between capital and total assets.

Unlock the intricacies of Basel III with our Introduction To Basel III .

Differences between Basel II and Basel III

Capital Requirements

Capital Requirements are a fundamental aspect of banking regulations, determining the minimum amount of capital that financial institutions must hold to ensure stability and mitigate risks. Capital Requirements Under Basel III were refined through Risk-weighted assets, tailoring capital allocation based on the riskiness of assets.

Basel III elevated this concept by introducing Capital Buffers - the Capital Conservation Buffer, Countercyclical Capital Buffer, and Systemically Important Banks (SIB) Buffer. These buffers act as protective cushions, ensuring banks have extra capital during economic stress. The evolution from Risk-based Capital Requirements in Basel II to the Comprehensive Capital Buffers in Basel III reflects the commitment to enhancing financial resilience and fortifying the global banking sector.

Risk Management

Risk Management is a fundamental aspect of banking regulations like Basel II and Basel III. In Basel II, Risk Management gained prominence as it introduced the concept of Risk-weighted assets, acknowledging that different assets carry varying levels of risk. This approach aimed to ensure that banks allocate capital more accurately based on the riskiness of their portfolios.

Basel III, building upon this foundation, extended Risk Management's scope to encompass not only credit, market, and Operational risks but also Liquidity risks. The introduction of Liquidity Standards and Leverage Ratios in Basel III enhances the banking sector's resilience against a wider range of risks, promoting a more stable and secure financial environment.

Liquidity and Funding

While Basel II laid the groundwork for Risk-based Capital Requirements, it did not explicitly address the critical aspect of Liquidity risk. This became glaringly evident during the 2008 financial crisis when many financial institutions struggled to access sufficient Liquidity, exacerbating the crisis.

As a response to the lessons learned from the crisis, Basel III Implementation introduced a paradigm shift by incorporating robust Liquidity Standards. The Liquidity Coverage Ratio (LCR) mandates banks to bear a minimum amount of high-quality liquid assets to meet short-term Liquidity needs during stressed scenarios.

Additionally, the Net Stable Funding Ratio (NSFR) ensures that banks maintain a secure funding profile over the longer term, enhancing their overall Liquidity resilience. These measures collectively fortify the banking system against Liquidity-driven shocks and contribute to a more stable financial landscape.

Systemic Risk

Basel II, although an advancement in Risk Management, didn't explicitly address Systemic Risk, which became evident during the 2008 crisis. In contrast, Basel III took a more comprehensive approach by introducing the Systemically Important Banks (SIB) Buffer. This buffer requires globally significant banks to hold extra capital, minimising the potential impact of their failure on the broader financial system.

This proactive measure is a critical enhancement that showcases Basel III's commitment to mitigating Systemic Risks and safeguarding the overall stability of the global financial ecosystem.

Timing and Implementation

The timing and Implementation of Basel II and Basel III reflect their contexts and responses to the evolving financial landscape. Basel II was introduced in 2004, before the 2008 financial crisis, with a focus on refining Risk Management practices. However, it faced criticism for not adequately addressing Liquidity and Systemic Risks.

In contrast, Basel III emerged as a direct response to the crisis, introduced gradually from 2010 onwards. Its phased implementation allowed banks time to adapt and adjust to the stricter Capital Requirements, Capital Buffers, and Liquidity standards. This approach acknowledged the need for a comprehensive regulatory response to systemic vulnerabilities, underscoring the importance of learning from past crises to shape more resilient financial frameworks.

Stay ahead in finance - Register now in our Introduction to Basel IV Training .

Impact on the banking landscape

The introduction of both Basel II and Basel III has left a lasting impact on the global banking landscape, reshaping the way financial institutions operate, manage risks, and ensure stability.

Basel II's impact

Basel II ushered in a new era of Risk-based Capital Requirements and enhanced Risk Management practices. By introducing Risk-weighted assets and differentiating Capital Requirements based on risk profiles, banks were incentivised to adopt more sophisticated Risk Assessment strategies. This led to improved Risk Management models, better allocation of capital, and a heightened focus on internal controls. The increased transparency facilitated by Basel II's Market Discipline pillar bolstered investor confidence and fostered more informed decision-making

Basel III's impact

Basel III's impact on the banking landscape is even more profound. The emphasis on Capital Buffers, Liquidity Standards, and Leverage Ratios has significantly improved the resilience of banks. The buffers act as shock absorbers, ensuring that banks have sufficient capital to withstand economic downturns without resorting to government bailouts.

The introduction of Liquidity Standards addresses a critical vulnerability exposed during the 2008 financial crisis, ensuring that banks maintain adequate Liquidity to navigate stress periods. Moreover, the Leverage Ratio guards against excessive borrowing, preventing undue risk-taking and enhancing overall stability.

Collectively, both frameworks have elevated Risk Management practices, ensuring that banks are better equipped to manage unexpected challenges. The regulatory changes have shifted banks' focus from mere compliance to a proactive approach that prioritises stability, Risk Assessment, and prudent management.

While Basel II refined Risk Assessment, Basel III Buffers have redefined the concept of banking resilience, introducing more robust measures to ensure stability in the face of economic stress. As the banking sector continues to evolve, the lessons learned from Basel II and Basel III will continue to influence regulatory frameworks and shape a more secure and resilient financial landscape.

Conclusion

In the continuum of banking regulations, Basel II and Basel III represent significant milestones in the pursuit of financial stability. While Basel II laid the foundation for Risk-based Capital Requirements, Basel III responded to the lessons of the 2008 crisis by introducing robust buffers and Liquidity Standards. The comparison between Basel II vs Basel III underscores the evolution of regulatory priorities, with Basel III setting a higher bar for capital adequacy, Liquidity, and Risk Management.

Navigate the world of Compliance with confidence. Register now in our Compliance Training.

Upcoming ISO & Compliance Resources Batches & Dates

Date

PCI DSS Implementer

PCI DSS Implementer

PCI DSS Implementer

Thu 3rd Apr 2025

PCI DSS Implementer

Thu 5th Jun 2025

PCI DSS Implementer

Thu 7th Aug 2025

PCI DSS Implementer

Thu 2nd Oct 2025

PCI DSS Implementer

Thu 4th Dec 2025

If you wish to make any changes to your course, please

If you wish to make any changes to your course, please