Top Rated Course

Top Rated Course

We may not have the course you’re looking for. If you enquire or give us a call on 01344203999 and speak to our training experts, we may still be able to help with your training requirements.

What is Credit Risk? A Comprehensive Overview

Eliza Taylor 22 February 2025Explore the intricacies surrounding Credit Risk through our comprehensive blog What is Credit Risk. Uncover the multifaceted evaluation of a borrower’s financial reliability, exploring the key factors like credit history, capacity, collateral, capital, and external conditions.

Training Outcomes Within Your Budget!

We ensure quality, budget-alignment, and timely delivery by our expert instructors.

Imagine you lend some money to your friend, expecting them to pay you back with interest. But what if they don't? What if they run away, or go bankrupt, or simply forget about their promise? That's what Credit Risk is all about: the chance of losing your hard-earned money because someone else fails to honour their debt obligations. Credit Risk is everywhere in the world of finance, affecting lenders, investors, and financial institutions. In this blog, we will explore What is Credit Risk, how it is measured, and how it can be managed effectively.

Table of Contents

1) Understanding What is Credit Risk

2) Methods for calculating Credit Risk

3) 5 C’s of Credit

4) Additional risks associated with bond investments

5) Conclusion

Understanding What is Credit Risk

Credit Risk refers to the potential loss that a lender may incur due to the failure of a borrower to repay a loan or meet their financial obligations. It is a crucial aspect of financial management and lending practices, as it assesses the likelihood of borrowers defaulting on their payments. Lenders, such as banks or financial institutions, evaluate Credit Risk before extending loans to individuals or businesses.

Furthermore, several factors contribute to Credit Risk assessment, including the borrower's Credit history, financial stability, income, and overall ability to meet debt obligations. Credit Risk management involves the development of strategies to mitigate potential losses, such as setting appropriate interest rates, establishing Credit limits, and implementing risk monitoring systems.

Moreover, Credit Risk is an inherent part of the lending and financial industry, and effective risk management is essential for maintaining the stability of financial institutions. Various tools and models, including Credit scoring and risk analytics, are employed to quantify and manage Credit Risk.

Additionally, diversification of loan portfolios and the use of collateral are common risk mitigation strategies. Successful Credit Risk management not only safeguards the interests of lenders but also contributes to the overall stability of the financial system.

Methods for calculating Credit Risk

The calculation of Credit Risk is vital for lenders to assess the likelihood of borrowers defaulting on loans. It involves evaluating factors like Credit history and financial stability. Effective risk assessment guides lending decisions, sets appropriate interest rates, and ensures financial stability by preventing potential losses, benefiting both lenders and the overall financial system.

Here are the key methods that you can utilise for the calculation of Credit Risk:

Evaluation of Assets Under Management

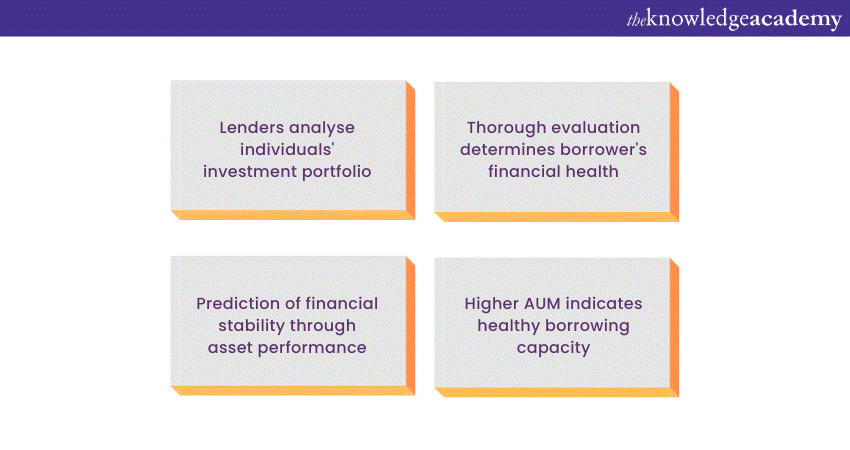

Evaluating Assets Under Management (AUM) is a critical component of calculating Credit Risk as it provides insights into a borrower's financial strength and ability to meet obligations. To assess AUM, lenders analyse an individual or business's investment portfolio, including stocks, bonds, and other assets.

Now such an evaluation helps determine the borrower's liquidity, diversification, and overall financial health. Lenders often consider the type of assets, their market value, and the level of risk associated with the investment portfolio.

Additionally, understanding the historical performance of these assets can provide valuable context for predicting future financial stability. A higher AUM may indicate a borrower's capacity to withstand economic downturns and fulfil financial obligations, reducing Credit Risk.

This comprehensive assessment of assets under management enables lenders to make informed decisions, set appropriate Credit limits, and establish terms that align with the borrower's financial profile.

Stand Out in Your Interview! Review these Credit Controller Interview Questions and step into your next interview with confidence.

Examination of Insurance Factors

Examining insurance factors is a crucial aspect of calculating Credit Risk, offering insights into a borrower's risk mitigation strategies. Lenders assess various insurance aspects, such as the type and coverage of policies held by individuals or businesses. This evaluation helps gauge the borrower's ability to manage unexpected financial challenges, reducing the likelihood of default.

Key factors include the comprehensiveness of coverage, policy terms, and the financial strength of the insurance provider. A borrower with well-structured insurance, covering potential risks, demonstrates a proactive approach to financial responsibility.

Moreover, lenders consider insurance factors alongside other risk indicators to make informed lending decisions, set appropriate interest rates, and establish Credit limits. This multifaceted examination of insurance factors enhances the overall risk management strategy, contributing to a more accurate assessment of Credit Risk and promoting financial stability in lending practices.

Assessment of Potential Return on Investment

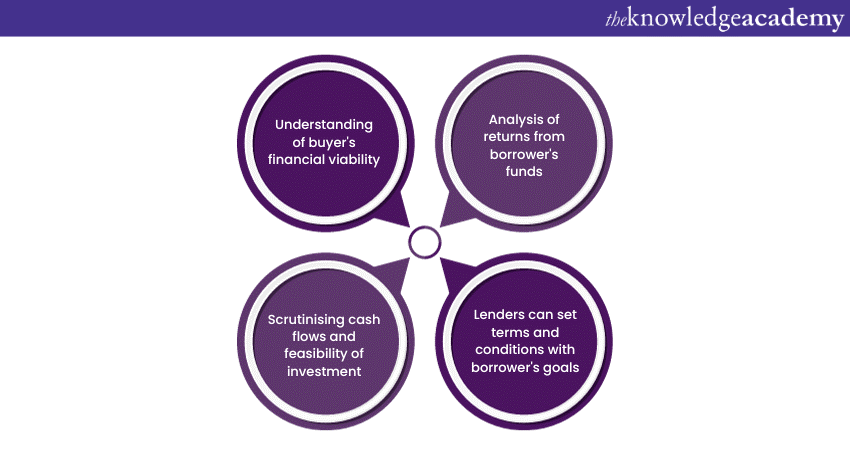

Assessing the potential Return on Investment (ROI) is integral to calculating Credit Risk, as it provides a comprehensive understanding of a borrower's financial viability and repayment capacity. Lenders analyse the prospective returns from the borrower's intended use of funds, considering factors such as business plans, investment projects, or asset acquisition.

This assessment involves scrutinising the expected cash flows, profitability projections, and the overall feasibility of the proposed investment. A positive ROI indicates the borrower's ability to generate income and meet financial obligations, lowering Credit risk. Conversely, a questionable or negative ROI raises concerns about the borrower's capacity to repay debt.

Now by evaluating potential ROI, lenders can make informed decisions, set appropriate terms and conditions, and align Credit offerings with the borrower's financial goals. This proactive approach enhances risk management strategies, ensuring a more accurate and holistic calculation of Credit Risk in the lending process.

Scrutiny of Debt Covenants

Scrutinising debt covenants is a critical step in calculating Credit Risk, offering lenders a detailed understanding of a borrower's financial discipline and adherence to contractual obligations. Debt covenants are stipulations within loan agreements that outline specific conditions and limitations borrowers must meet.

Additionally, lenders rigorously examine these covenants to assess the borrower's financial health, risk tolerance, and ability to honour contractual commitments. The key aspects of scrutiny include evaluating leverage ratios, liquidity requirements, and restrictions on additional debt.

A breach of these covenants may signal financial distress and an increased risk of default. By thoroughly analysing debt covenants, lenders can proactively identify potential challenges, adjust lending terms accordingly, and implement risk mitigation strategies.

More importantly, this form of meticulous examination enhances the accuracy of credit risk calculations, promoting sound lending practices and safeguarding the interests of financial institutions.

Learn to apply principles of Financial Management by signing up for our Financial Management Course now!

5 C’s of Credit

The 5 C's of Credit are a fundamental framework used by lenders to assess a borrower's creditworthiness and improve credit score. Character examines credit history, Capacity evaluates repayment ability, Collateral provides security, Capital assesses financial stake, and Conditions consider external factors.

This holistic approach guides informed lending decisions and risk management strategies. Here are the 5 C’s of Credit explained in further detail:

1) Character

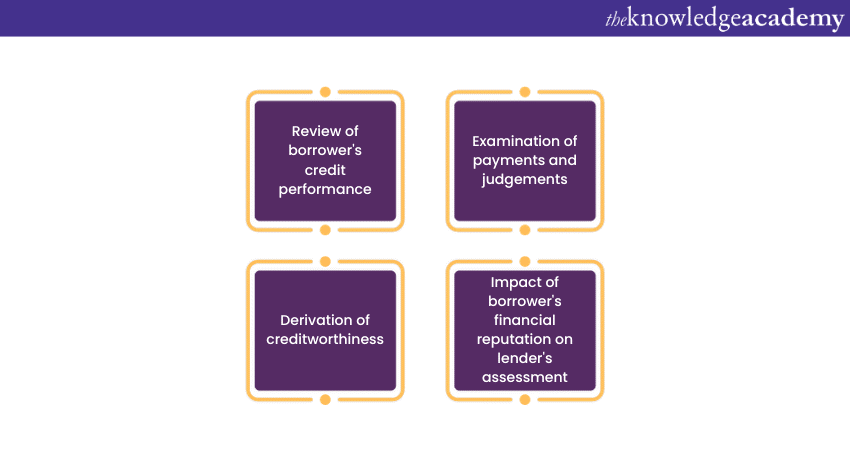

Character refers to the borrower's Credit history and reputation for repaying debts. It assesses the individual's or business's trustworthiness and reliability in meeting financial obligations. Character comprises of three key components, which are as follows:

a) Credit history: Lenders review the borrower's past credit performance, examining factors such as timely payments, defaults, bankruptcies, and any outstanding judgments.

b) Credit score: A numerical representation of creditworthiness derived from credit reports. Higher scores indicate better creditworthiness.

c) Reputation: The borrower's general financial reputation, including their integrity in financial dealings, can impact the lender's assessment.

2) Capacity

Capacity evaluates the borrower's ability to repay the loan by assessing their financial stability and income relative to existing and potential debt obligations. Capacity is comprised of three key components that are:

a) Income: Lenders analyse the borrower's income sources, stability, and consistency to determine if it is sufficient to cover debt repayments.

b) Debt-to-Income ratio (DTI): Calculated by dividing the borrower's total monthly debt payments by their gross monthly income. A lower DTI indicates a healthier financial situation.

c) Cash flow: Evaluating the borrower's cash flow helps lenders understand their ability to generate liquid funds for repayment.

3) Collateral

Collateral serves as security for the loan, providing a secondary source of repayment in case the borrower defaults. It adds a layer of protection for the lender. Collateral is comprised of three key components which are:

a) Types of Collateral: Assets such as real estate, vehicles, or business inventory can be pledged as collateral. The type of collateral accepted varies based on the loan type.

b) Valuation: Lenders assess the value of the collateral to ensure it is sufficient to cover the loan amount. Professional appraisals may be required.

c) Market conditions: Fluctuations in the market can impact the value of collateral, influencing the lender's risk assessment.

Find top FinOps Interview Questions and Answers to ensure you're ready for your next interview!

4) Capital

Capital refers to the borrower's equity or the financial stake they have in the business or investment. It demonstrates the level of commitment and risk the borrower is willing to undertake. The three key components of Capital are as follows:

a) Owner's equity: In a business context, this represents the owner's investment in the business. A higher equity stake indicates a greater commitment to the venture.

b) Retained earnings: For established businesses, retained earnings contribute to capital. It reflects the company's profitability and reinvestment in its own growth.

c) Liquidity: The borrower's access to liquid assets, such as cash, that can be used to meet financial obligations in the short term.

5) Conditions

Conditions encompass the external factors that may impact the borrower's ability to repay the loan. Lenders consider economic conditions, industry trends, and the purpose of the loan. The Conditions aspect of Credit comprises of the following key parts:

a) Economic Conditions: Lenders assess the overall economic environment to gauge its potential impact on the borrower's financial stability and ability to repay.

b) Industry Trends: Specific conditions within the borrower's industry can influence the risk associated with the loan. Lenders consider the outlook and challenges of the relevant sector.

c) Loan Purpose: The intended use of funds plays a role. For example, a loan for business expansion may be viewed differently than one for debt consolidation.

Acquire the knowledge of using Credit letters effectively by signing up for The Letters of Credit Training now!

Additional risks associated with bond investments

Bond investments carry various additional risks. Interest rate risk arises from fluctuations impacting bond prices. Inflation risk threatens the real value of fixed payments due to rising prices.

Moreover, Call risk involves issuers redeeming bonds prematurely, potentially limiting returns. Understanding and managing these risks are crucial for informed bond investment decisions. Here are the three key risks described as follows:

Interest rate risk

Interest rate risk is a significant factor affecting bond investments, closely tied to Credit Control. This risk arises from the inverse relationship between bond prices and interest rates. When interest rates rise, the value of existing bonds tends to fall, and vice versa.

This is because newly issued bonds with higher interest rates become more attractive to investors than older bonds with lower rates. Long-term bonds are particularly susceptible to interest rate fluctuations, exposing investors to potential capital losses if they sell their bonds before maturity. Managing interest rate risk involves carefully considering the investment's duration and the prevailing interest rate environment.

Inflation risk

Inflation risk, also known as purchasing power risk, is the threat that inflation will erode the real value of future bond payments. Fixed-rate bonds provide a predetermined interest income, and if inflation accelerates, the purchasing power of those fixed payments diminishes.

Investors face the risk of their returns not keeping pace with the rising cost of living. To mitigate inflation risk, investors may consider inflation-protected securities or bonds with floating interest rates that adjust with inflation. These instruments provide a degree of protection against the eroding effects of inflation on the purchasing power of bond income.

Call risk

Call risk is associated with bonds that have callable features, meaning the issuer can redeem or ‘call’ the bonds before maturity. When interest rates decline, issuers may choose to call existing bonds and refinance at lower rates, leaving investors with the return of principal but potentially limiting the upside of holding higher-yielding bonds.

This risk is more pronounced in a declining interest rate environment. Investors exposed to call risk may experience reinvestment challenges, as the replacement bonds may offer lower yields. Assessing the call provisions of a bond and considering the issuer's likelihood of exercising this option is crucial for investors to make informed decisions and manage call risk effectively.

Stand out in the finance industry by developing strong Credit Controller Skills. Discover how to get started!

Conclusion

In conclusion, we hope that you have understood what Credit Risk is and how it is paramount for prudent financial management. This comprehensive overview highlights its multifaceted nature, encompassing factors like credit history, capacity, collateral, capital, and conditions. Navigating these elements empowers informed lending decisions, promoting stability and resilience in the financial domain, which can also be a focus in Credit Controller Interview Questions.

Equip yourself with the fundamentals of Credit assessment by signing up for our Introduction to Credit Control Course now!

Frequently Asked Questions

What are the Other Resources and Offers Provided by The Knowledge Academy?

The Knowledge Academy takes global learning to new heights, offering over 3,000 online courses across 490+ locations in 190+ countries. This expansive reach ensures accessibility and convenience for learners worldwide.

Alongside our diverse Online Course Catalogue, encompassing 19 major categories, we go the extra mile by providing a plethora of free educational Online Resources like News updates, Blogs, videos, webinars, and interview questions. Tailoring learning experiences further, professionals can maximise value with customisable Course Bundles of TKA.

Upcoming Accounting and Finance Resources Batches & Dates

Date

Introduction to Credit Control

Introduction to Credit Control

Introduction to Credit Control

Fri 9th May 2025

Introduction to Credit Control

Fri 11th Jul 2025

Introduction to Credit Control

Fri 12th Sep 2025

Introduction to Credit Control

Fri 14th Nov 2025

If you wish to make any changes to your course, please

If you wish to make any changes to your course, please