Top Rated Course

Top Rated Course

We may not have the course you’re looking for. If you enquire or give us a call on +971 8000311193 and speak to our training experts, we may still be able to help with your training requirements.

Inventory Accounting: Methods, Benefits, & How it Works

Sophia Ellis 26 November 2024Inventory Accounting handles the values of a company's inventory, including raw materials, work-in-progress, and finished goods. It decides the cost of goods sold and oversees stock levels. This blog discusses what Inventory Accounting is, how it works, advantages and some examples of Inventory in Accounting.

Training Outcomes Within Your Budget!

We ensure quality, budget-alignment, and timely delivery by our expert instructors.

Table of Contents

Picture an inventory warehouse filled with raw materials, in-progress goods, and finished products ready to hit the market. Each item represents a potential sale and a critical part of your business's financial puzzle. This is where Inventory Accounting plays a crucial role in tracking inventory costs, managing stock levels, and ensuring accurate financial reporting. It can turn your stock into a strategic asset, optimising operations, cutting costs, and driving profitability. Sounds good!

Let’s explore Inventory Accounting, its workings, methods, advantages, and some real-world examples.

Table of Contents

1) What is Inventory Accounting?

2) How Inventory Accounting Works?

3) Methods of Inventory Accounting

4) Advantages of Inventory Accounting

5) Examples of Inventory in Accounting

6) Inventory Accounting Software

7) Conclusion

What is Inventory Accounting?

Inventory accounting is the process of valuing and tracking a company’s inventory throughout its lifecycle, from acquisition to sale. It involves recording the costs associated with purchasing, producing, and storing goods, as well as accounting for changes in inventory levels. Accurate inventory accounting helps businesses determine their cost of goods sold (COGS), manage stock levels efficiently, and assess profitability. There are different methods used in inventory accounting, such as FIFO (First In, First Out), LIFO (Last In, First Out), and weighted average cost, each impacting financial statements differently.

In retail, Inventory Accounting typically covers three types of inventory or production stages:

a) Raw materials

b) In progress items

c) Final products ready for sale

The unsold inventory must be considered as an asset in end-of-year financial records. The goal is to monitor both the cost of sold inventory and the value of unsold inventory at the end of each accounting term.

Changes in the value of goods affect your inventory value, which in turn changes the overall value of your business.

How Inventory Accounting Works?

Inventory Accounting helps the company by minimising costs and optimising its stock levels. Now, let's understand the working of Inventory Accounting step-by-step:

1) Inventory Estimation: Decide the inventory value by selecting a valuation method like First-In, First-Out (FIFO), Last-In, First-Out (LIFO), or Weighted Average Cost.

2) Recording Transactions: Track inventory purchases, sales, and adjustments in the accounting system to ensure inventory levels are correct.

3) Cost of Goods Sold (COGS): Decide on COGS by selecting a valuation method that affects the gross profit and financial reports of the company.

4) Regular Inventory Counts: Schedule regular physical stock counts to compare actual inventory levels with tracked data.

5) Adjustments: Make necessary changes for shrinkage, obsolescence, or damage to maintain accurate inventory values.

Reporting: Recording inventory values in financial reports impacts essential metrics such as profit and liquidity.

Transform your Inventory with our Inventory Accounting and Costing Course – Join now!

Methods of Inventory Accounting

Inventory Accounting techniques determine the timing and way income and costs are documented in financial reports. Given below are the two main methods used:

1) Cash Basis Inventory Accounting

In this method, transactions are recorded when cash is exchanged upon purchasing or selling inventory. It is best for smaller businesses with fewer transactions as it focuses on cash flow rather than accruals.

However, it can provide incorrect data on financial health as it doesn't involve unpaid bills and uncollected revenue. Businesses with complex inventory may find it less suitable.

2) Accrual Basis Inventory Accounting

In this method, transactions are recorded when they occur, irrespective of the cash flow. It records a purchase when sales are delivered, even if the payment has not been made. Compared to cash-basis Inventory Accounting, it offers a more precise and more accurate picture of a company's financial health.

Furthermore, it provides detailed insights into profitability. The only drawback is the use of complex tracking and strict regulations.

Advantages of Inventory Accounting

Inventory Accounting is crucial when managing a company's financial health by accurately monitoring costs. Here are some of the key advantages of it:

a) Accurate Financial Reporting: Inventory Accounting reflects a company’s assets and helps calculate COGS and gross profit. This accuracy generates reliable financial statements, which are important for regulatory compliance and stakeholders.

b) Better Inventory Management: Better Inventory Management allows businesses to optimise their stock levels, reduce costs, and avoid overstocking. It even streamlines operations and minimises waste, leading to enhanced profitability.

c) Cost Control: Inventory Accounting can identify cost variances and trends, enabling companies to control costs. Businesses can work on inventory data to make informed decisions on pricing, purchasing, and developing production tactics.

d) Enhanced Cash Flow Management: Effective Inventory Accounting manages cash flow by identifying the capital linking to stocks. Businesses can understand their inventory flow and ensure they possess enough liquidity for operations.

e) Tax Benefits: Methods like FIFO and LIFO can affect recorded income and taxes a business owes. Companies can utilise these methods to minimise tax liabilities.

f) Improved Decision-Making: Detailed inventory records offer insights into product performance, customer demand, and sales patterns. These insights help make better decisions that drive business growth.

Master Accounting basis with our Accounting Course – Register now!

Examples of Inventory in Accounting

Let’s see some real-work examples in retail and manufacturing context, to make our understanding of inventory models clearer.

a) Raw Materials/Components: The raw materials for a T-shirt manufacturer consist of fabric, thread, dyes, and print designs.

b) Finished Goods: A jeweller makes charming necklaces. Workers tie necklaces onto preprinted cards and place them in envelopes, producing final products ready for purchase. Packaging and labour expenses are part of the cost of goods sold.

c) Work in Progress (WIP): A cell phone assembly includes various parts, like the body and motherboard, at a specific work area. Items currently being assembled are classified as work in progress.

d) Maintenance, Repair, and Operations (MRO) Goods: An MRO inventory for a condo community consists of supplies such as copy paper, folders, printer toner, gloves, glass cleaner, and brooms for ground maintenance.

e) Packing Materials: A seed company uses sealed bags as the main packaging for items such as flax seeds. The bags are then put into boxes for transportation, and the boxes are secured on pallets with shrink wrap.

f) Anticipated/Smoothing Inventory: An event planner buys discounted ribbon spools and floral tablecloths for an upcoming busy June wedding season.

g) Decoupled Inventory: In a bakery, decorators have a stock of sugar roses for decorating wedding cakes. This reserve enables them to continue decorating even if other supplies, such as frosting mix, are delayed.

h) Service Inventory: A restaurant has ten tables and is open for 12 hours daily. Customers typically spend an hour waiting for their meal, which is equivalent to 120 meals in its inventory.

i) Transit Inventory: An art store ordered 40 tins of a popular pencil set. The tins, which are currently being shipped from the vendor, are considered transit inventory.

j) Excess Inventory: A shampoo company manufactures 50,000 limited-edition bottles for the Olympics but only sells 45,000. The leftover bottles, labelled for an already-occurring event, turn into a surplus stock that might require a discount or disposal.

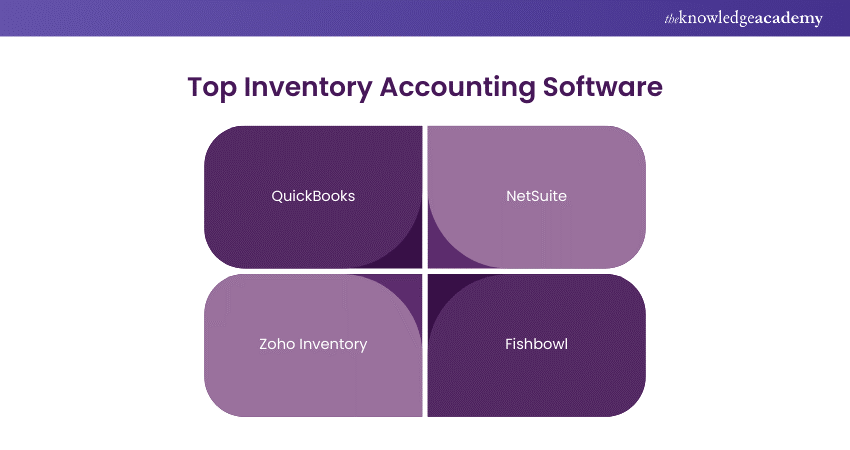

Inventory Accounting Software

Effective management of inventory requires the right Inventory Accounting software. Here are the top ones:

a) QuickBooks: QuickBooks combines Inventory Management with accounting, making it perfect for small to medium businesses. It comes with an easy-to-use interface and delivers functions such as immediate inventory updates and thorough reporting.

b) NetSuite: NetSuite provides a robust cloud-based solution with advanced features like order management, demand planning, supply chain automation, etc. It’s perfect for large enterprises.

c) Zoho Inventory: It is a cost-effective inventory solution that comes with features like real-time tracking, order management, and multi-channel selling.

d) Fishbowl: Fishbowl is suitable for distributors, wholesalers, and manufacturers. It can be integrated with QuickBooks for inventory tracking, manufacturing process management, and order management.

Select the right Inventory Accounting software based on your business size, specific needs, and industry type.

Conclusion

Inventory Accounting is vital for accurately managing a company's financial health and optimising inventory control. Businesses can make informed decisions by documenting costs and stock levels, lowering waste, and improving cash flow. Methods like FIFO, LIFO, or Weighted Average offer valuable insights into inventory profitability and operational efficiency. Thus, businesses should invest in reliable Inventory Accounting practices and technologies to stay competitive.

Simplify your finances with our Bookkeeping Course – Sign up today!

Frequently Asked Questions

How Often Should Inventory be Reviewed?

Inventory reviews should be done monthly or quarterly to maintain accuracy and reduce costs.

What is the Weighted Average Cost method?

It refers to the ratio of the cost of goods available for sale to the number of units available for sale. Most companies utilise the weighted average method to assign costs to inventory.

How can Technology Improve Inventory Accounting?

Technology enhances Inventory Accounting by reducing errors, offering real-time data and automating tracking for smooth management and reporting.

What are the Other Resources and Offers Provided by The Knowledge Academy?

The Knowledge Academy takes global learning to new heights, offering over 30,000 online courses across 490+ locations in 220 countries. This expansive reach ensures accessibility and convenience for learners worldwide.

Alongside our diverse Online Course Catalogue, encompassing 19 major categories, we go the extra mile by providing a plethora of free educational Online Resources like News updates, Blogs, videos, webinars, and interview questions. Tailoring learning experiences further, professionals can maximise value with customisable Course Bundles of TKA.

What is The Knowledge Pass, and How Does it Work?

The Knowledge Academy’s Knowledge Pass, a prepaid voucher, adds another layer of flexibility, allowing course bookings over a 12-month period. Join us on a journey where education knows no bounds.

What are the Related Courses and Blogs Provided by The Knowledge Academy?

The Knowledge Academy offers various Accounting Courses, including the Inventory Accounting And Costing Course, Fixed Assets Accounting And Management Course, and Accounting Course. These courses cater to different skill levels, providing comprehensive insights into What is Management Accounting.

Our Accounting and Finance Blogs cover a range of topics related to Finance, offering valuable resources, best practices, and industry insights. Whether you are a beginner or looking to advance your Accounting skills, The Knowledge Academy's diverse courses and informative blogs have got you covered.

Upcoming Accounting and Finance Resources Batches & Dates

Date

Inventory Accounting and Costing Course

Inventory Accounting and Costing Course

Inventory Accounting and Costing Course

Fri 28th Feb 2025

Inventory Accounting and Costing Course

Fri 4th Apr 2025

Inventory Accounting and Costing Course

Fri 27th Jun 2025

Inventory Accounting and Costing Course

Fri 29th Aug 2025

Inventory Accounting and Costing Course

Fri 24th Oct 2025

Inventory Accounting and Costing Course

Fri 5th Dec 2025

If you wish to make any changes to your course, please

If you wish to make any changes to your course, please